Norway's Sovereign Wealth Fund is Europe's Missing Venture Capitalist

Elif Memet, Erik Dalaker, Julian von Moltke, Adrien Joly / Apr 21, 2026

Europe has the ideas and the talent but it lacks risk capital at scale. One institution could supply such capital: Norway's sovereign wealth fund. At nearly two trillion euros, the largest sovereign fund in the world, it could anchor a dedicated European venture vehicle that crowds in private capital where it is currently scarce.

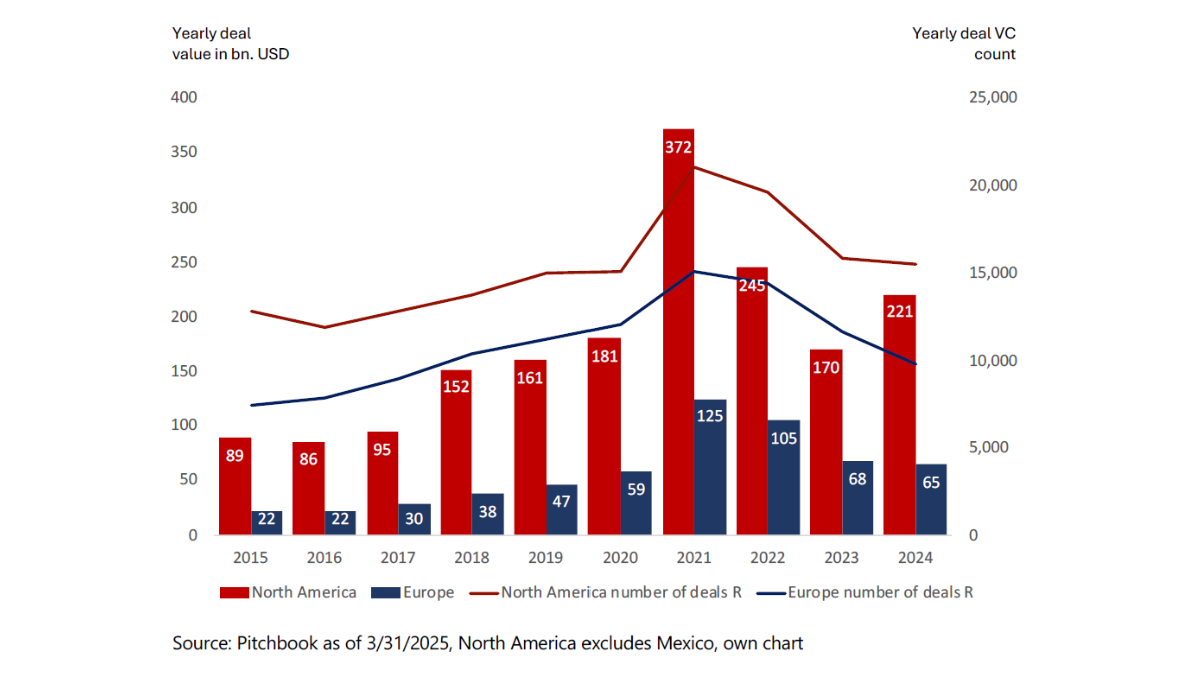

In the share of global scientific citations, Europe and the United States are near parity. And backing such talent pays off. European venture funds — private investors willing to finance risky, early-stage startups — have outperformed North American funds for the last fifteen years. Yet the average deal in North America is three times larger than in Europe, and the number of unicorns five times higher. If the talent and research are there — and if the funds that do invest perform well — why does Europe still produce fewer and less scaled startups?

Europe seems stuck in a structural trap: it needs venture capital markets to support innovation, but without innovation, there are not enough investment opportunities for large venture funds to deploy capital at scale.

For years, Brussels has talked about a capital markets union. Mario Draghi’s 2024 competitiveness report revived that ambition, calling for Europe, among others, to redirect household savings towards productive assets. More than a year later, there has been little progress on mobilizing capital at the scale the challenge demands. There is little doubt that much of Europe’s funding gap stems from overregulation, weak procurement, and fragmented market integration. But even if capital markets were fully integrated tomorrow, innovation needs something more: an ecosystem.

In the United States, the world’s most developed capital market, venture capital markets are ecosystems. Silicon Valley plays a game built on relationships, concentration, and size. Over the past decade, a few venture funds have raised most of the available capital. These investors do more than provide funding. They connect founders to clients, talent, and follow-on capital. Founders are encouraged to “fail fast,” and those who fall short the first time are often backed again when they return with a stronger idea.

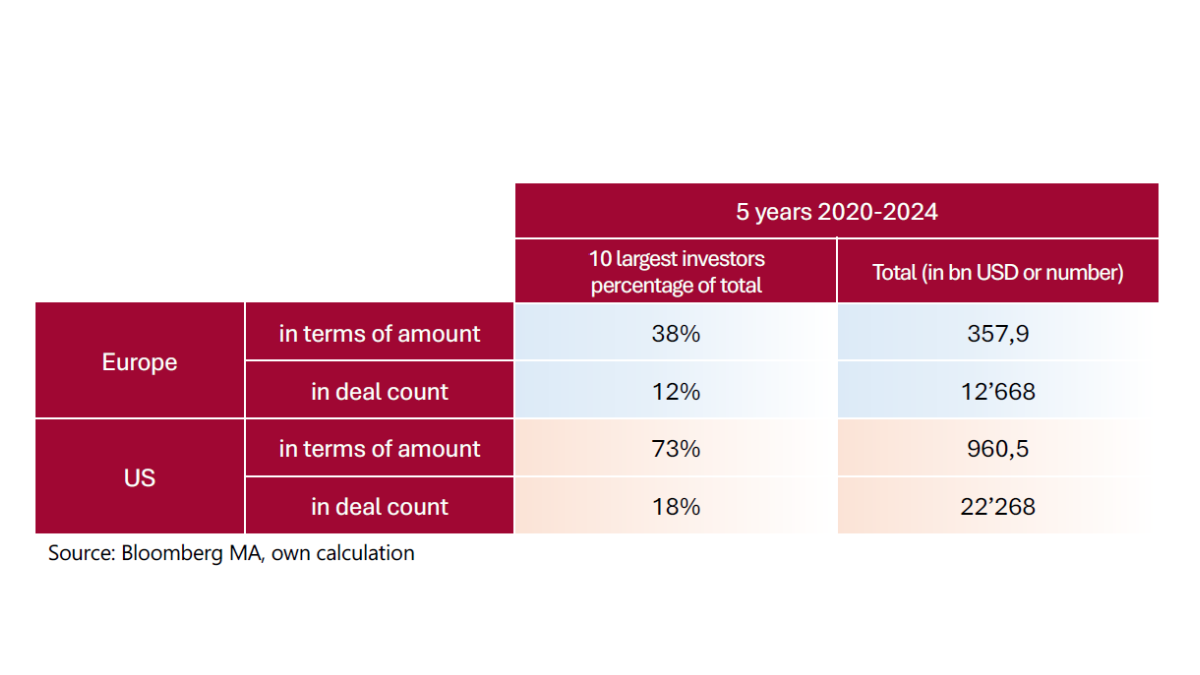

The difference is visible in the market structure. In the US, the ten largest investors accounted for 73 percent of venture deal value. In Europe, the ten largest accounted for almost half of that, 38 percent.

The solution for European innovation lies farther north than the EU expects. Among Europe’s many financial actors, one stands out as able to provide the critical spark: Norway’s sovereign wealth fund. Formally the Government Pension Fund Global (GPFG), managed by Norges Bank Investment Management (NBIM), is the largest sovereign wealth fund in the world, with assets nearing two trillion euros. With its balance sheet, investment horizon, and governance capacity, even a small portion of its funds could anchor European venture capital.

A dedicated venture fund managed by NBIM investing directly and exclusively in European start-ups would crowd in capital where it is currently scarce, as private European asset managers could then scale their own commitments alongside NBIM’s new vehicle.

Even a modest allocation of two percent of NBIM’s assets, approximately 40 billion euros, to such a new venture capital entity, would send a market signal stronger than any policy communiqué about a capital markets union: a credible, patient investor is ready to finance innovation in Europe.

Let’s look at the business case for Norway. Its peers, from sovereign wealth funds like Abu Dhabi’s Mubadala investment company to pension funds like California Public Employees' Retirement System (CalPERS), routinely allocate more than 20 percent of their assets towards private equity and venture capital. With annualized venture returns near 20 percent, this strategy has worked. Sure, NBIM could say that the current governance structure of GPFG doesn’t allow significant allocation to venture capital and that the discipline behind its current model is exactly what made it the largest sovereign wealth fund in the world. All true. But both new asset classes and separate entities have been added in the past. And what if this strategy leads to improved returns, just as it did for its peers?

Equally important is the geopolitical case. In a new multipolar world, Norway and the European Union should seek closer ties, and for this, financial capacity across the continent is as crucial as defense cooperation. Yet, much of that capacity is concentrated elsewhere. Currently, nine out of the 10 of the Norwegian Sovereign Wealth Fund’s largest investment positions are in US companies, with 56 percent of the fund's equity invested in North America, compared to only 22 percent in Europe.

A greater regional allocation would help rebalance the fund’s exposure towards Europe, while also placing Norway at the center of European innovation financing. This is not an argument for Norway to weaken its transatlantic ties or give up its benchmark-anchored global investment strategy. But it does invite a strategic assessment: should the fund be more deliberate about how its capital is distributed?

What might this look like in practice? A phased deployment — beginning with co-investments alongside established venture funds before scaling toward direct commitments — would allow NBIM to build expertise without abandoning its fiduciary discipline. Structural safeguards could include strict return benchmarks and co-investment requirements with private investors. Practical questions such as size, structure, governance, and investment model are manageable.

The remaining obstacle is political. Any substantial change to the funds mandate and structure needs to be approved in parliament. So far, the Norwegian Government has rejected multiple calls by experts and, even NBIM’s own CEO, to advance investments in private equity and, thereby, venture capital. Amid changing geopolitical realities and yet another committee of experts recommending NBIM to open for private equity investments earlier this year, we believe it is time for the Norwegian government to reconsider its position. Norway and Europe cannot afford inaction.

Critics will argue that a sudden availability of large amounts of capital could inflate valuations or flow to companies that are not the best innovators. They are right. But it is a cost worth paying in the short run, as this is precisely the design of the venture capital model. It relies on a portfolio of imperfect bets in pursuit of rare breakthroughs. What matters most is setting the flywheel in motion.

Where might this flywheel take us? NBIM would invest in companies attempting true productivity-transformation, not projects of national vanity. For this is the ultimate source of economic value and power. Take foundational AI: the capital, compute, and talent advantages of the incumbents are steep, and catching up to lead the frontier is a questionable use of European resources today. However, in next-generation technologies, such as quantum, advanced materials, or synthetic biology, the frontier remains open, and the value to be derived is large. While the United States and China battle for the lead here, too, no one has lapped the field yet. European investment can still buy a seat at the frontier, not just a ticket to follow.

Europe has an abundance of knowledge and ideas, but translating them into economic and technological power requires a commensurate abundance of capital. Capital is the prerequisite for scaling European technologies, and investors such as NBIM should take the lead.

***

The piece relies upon research conducted at Harvard under the guidance of Helena Malikova, CFA, Fellow at Harvard Kennedy School of Government’s Carr Center for Human Rights. Malikova is an EU civil servant; the opinions expressed in this article are solely the opinions of the authors. To the extent that Malikova provided guidance, her guidance does not reflect an official position of the European institutions.

Authors